Euronext N.V. (short for European New Exchange Technology) is the largest stock exchange in Europe, operating markets in Amsterdam, Brussels, Dublin, Lisbon, London, Oslo and Paris. As of June 2020, it had nearly 1,500 listed issuers worth €3.8 trillion in market capitalisation.

Euronext operates regulated equity and derivatives markets and is the largest centre for debt and funds listings in the world. Its product range includes equities, exchange-traded funds, warrants and certificates, bonds, derivatives, commodities and indices as well as a foreign exchange trading platform. Euronext also provides technology and managed services to third parties. In addition to its main regulated market, it operates Euronext Growth and Euronext Access, providing access to listing for small and medium-sized enterprises. Euronext provides custody and settlement services through central securities depositaries (CSD) in Denmark, Norway and Portugal.

Euronext’s registered office and corporate headquarters are situated in Amsterdam and Paris, respectively.

Tracing its origins back to the founding of the Amsterdam Stock Exchange in 1602 by the Dutch East India Company, Euronext was founded in 2000 by the merger of the exchanges in Amsterdam, Paris and Brussels. Euronext has since grown by developing services and acquiring additional exchanges and has, after being merged with the New York Stock Exchange (NYSE) from 2007 to 2014 as NYSE Euronext, been spun off to once again being a standalone European exchange. Since its IPO in 2014, Euronext has expanded its European footprint and diversified its revenue streams by acquiring FastMatch, (now Euronext FX) a global FX spot market operator, in 2017, the Irish Stock Exchange in 2018 (now Euronext Dublin), Oslo Børs VPS, the owner of the Norwegian stock exchange in 2019, and announced in October 2020 that it has entered into a binding agreement with the London Stock Exchange Group (LSEG) to acquire Borsa Italiana Group

Operations

Markets

In addition to its main regulated market, Euronext operates Euronext Growth and Euronext Access, multilateral trading facilities (MTFs) which provide access to listing for small and medium-sized enterprises.

Euronext markets as of September 2020

Market – Euronext – Euronext Growth – Euronext Access/Euronext Access +

Venues

Amsterdam, Brussels, Dublin, Lisbon, Oslo, Paris

Brussels, Dublin, Lisbon, Oslo, Paris

Brussels, Lisbon, Paris

Topology – EU regulated – MTF – MTF

Number of issuers 776 – 229 – 180

Avg. size at initial public offering €278.1m – €22.8m – €0.1m

Avg. market cap. at initial public offering €5,514m – €97m – €51m

Euronext maintains a single order book, and Optiq is the electronic trading platform it currently uses and develops. Optic has also been sold and is in use by a number of third party exchanges around the world.

Indices

Euronext manages various country (national), as well as pan-European regional and sector and strategy indices.

Flagship indices managed by Euronext

Flagship indices managed by Euronext

Name – Symbol – Trading Currency

European

European Union Euronext 100 N100 EUR

National

Netherlands AEX AEX EUR

Belgium BEL 20 BEL20 EUR

France CAC 40 PX1 EUR

Republic of Ireland ISEQ 20 ISEQ20 EUR

Portugal PSI 20 PSI20 EUR

Norway OBX 25 OBX NOK

Central securities depository

Euronext provides custody and settlement services through central securities depositaries (CSD) in Denmark, Norway and Portugal.

Foreign exhange trading

Euronext FX is a global foreign exchange trading platform, known as FastMatch until 2019.

Other

Euronext operates regulated equity and derivatives markets and is the largest centre for debt and funds listings in the world. Its product range includes equities, exchange-traded funds, warrants and certificates, bonds, derivatives and commodities.

Financial information

(amounts in millions)

Year – Revenue – EBITDA – Net result

2014 – €458,5 – €225,4 – €118,2

2015 – €518,5 – €283,8 – €172,7

2016 – €496,4 – €283,9 – €197,0

2017 – €532,3 – €297,8 – €241,3

2018 – €615,0 – €354,3 – €216,0

2019 – €679,1 – €399,4 – €222,0

History

The following timeline outlines the consolidation through mergers and acquisitions among bourses in the European Union, which has taken place since the 1990s in response to financial harmonisation and liberalisation. Current, independent (parent) exchange companies

Background: Pre-merger bourses

Amsterdam (1602–2000)

The Amsterdam Stock Exchange (Dutch: Amsterdamse effectenbeurs) was considered the oldest “modern” securities market in the world. It was shortly after the establishment of the Dutch East India Company (VOC) in 1602 when equities began trading on a regular basis as a secondary market to trade its shares. Prior to that, the market existed primarily for the exchange of commodities. In that year, the States General of the Netherlands granted the VOC a 21-year charter over all Dutch trade in Asia and quasi-governmental powers. The monopolistic terms of the charter effectively granted the VOC complete authority over trade defenses, war armaments, and political endeavors in Asia. The first multi-national corporation with significant resource interests was thereby established. In addition, the high level of risk associated with trade in Asia gave the VOC its private ownership structure. Following in the footsteps of the English East India Company, stock in the corporation was sold to a large pool of interested investors, who in turn received a guarantee of some future share of profits. In the Amsterdam East India House alone, 1,143 investors subscribed for over ƒ3,679,915 or €100 million in today’s money

The subscription terms of each stock purchase offered shareholders the option to transfer their shares to a third party. Quickly a secondary market arose in the East India House for resale of this stock through the official bookkeeper. After an agreement had been reached between the two parties, the shares were then transferred from seller to buyer in the “capital book”. The official account, held by the East India House, encouraged investors to trade and gave rise to market confidence that the shares weren’t just being transferred on paper. Thus, speculative trading immediately ensued and the Amsterdam securities market was born.

A big acceleration in the turnover rate came in 1623, after the 21-year liquidation period for the VOC ended. The terms of the initial charter called for a full liquidation after 21 years to distribute profits to shareholders. However, at this time neither the VOC nor its shareholders saw a slowing down of Asian trade, so the States General of the Netherlands granted the corporation a second charter in the West Indies.

This new charter gave the VOC additional years to stay in business but, in contrast to the first charter, outlined no plans for immediate liquidation, meaning that the money invested remained invested, and dividends were paid to investors to incentivize shareholding. Investors took to the secondary market of the newly constructed Amsterdam Stock Exchange to sell their shares to third parties. These “fixed” capital stock transactions amassed huge turnover rates, and made the stock exchange vastly more important. Thus the modern securities market arose out of this system of stock exchange.

The voyage to the precious resources in the West Indies was risky. Threats of pirates, disease, misfortune, shipwreck, and various macroeconomic factors heightened the risk factor and thus made the trip wildly expensive. So, the stock issuance made possible the spreading of risk and dividends across a vast pool of investors. Should something go wrong on the voyage, risk was mitigated and dispersed throughout the pool and investors all suffered just a fraction of the total expense of the voyage.

The system of privatizing national expeditions was not new to Europe, but the fixed stock structure of the East India Company made it one of a kind. In the decade preceding the formation of the VOC, adventurous Dutch merchants had used a similar method of “private partnership” to finance expensive voyages to the East Indies for their personal gain. The ambitious merchants pooled money together to create shipping partnerships for exploration of the East Indies. They assumed a joint-share of the necessary preparations (i.e. shipbuilding, stocking, navigation) in return for a joint-share of the profits. These Voorcompagnieën took on extreme risk to reap some of the rewarding spice trade in the East Indies, but introduced a common form of the joint-stock venture into Dutch shipping.

Although some of these voyages predictably failed, the ones that were successful brought promise of wealth and an emerging new trade. Shortly after these expeditions began, in 1602, the many independent Voorcompagnieën merged to form the massive Dutch East India Trading Company. Shares were allocated appropriately by the Amsterdam Stock Exchange and the joint-stock merchants became the directors of the new VOC. Furthermore, this new mega-corporation was immediately recognized by the Dutch provinces to be equally important in governmental procedures. The VOC was granted significant war-time powers, the right to build forts, the right to maintain a standing army, and permission to conduct negotiations with Asian countries. The charter created a Dutch colonial province in Indonesia, with a monopoly on Euro-Asian trade

The rapid development of the Amsterdam Stock exchange in the mid 17th century lead to the formation of trading clubs around the city. Traders met frequently, often in a local coffee shop or inns to discuss financial transactions. Thus, “Sub-markets” emerged, in which traders had access to peer knowledge and a community of reputable traders.

These were particularly important during trading in the late 17th century, where short-term speculative trading dominated. The trading clubs allowed investors to attain valuable information from reputable traders about the future of the securities trade.[26] Experienced traders on the inside circle of these trading clubs had a slight advantage over everyone else, and the prevalence of these clubs played a major role in the continued growth of the stock exchange itself.

Additionally, similarities can be drawn between modern day brokers and the experienced traders of the trading clubs. The network of traders allowed for organized movement of knowledge and quick execution of transactions. Thus, the secondary market for VOC shares became extremely efficient, and trading clubs played no small part. Brokers took a small fee in exchange for a guarantee that the paperwork would be appropriately filed and a “buyer” or “seller” would be found. Throughout the 17th century, investors increasingly sought experienced brokers to seek information about a potential counterparty.

The European Options Exchange (EOE) was founded in 1978 in Amsterdam as a futures and options exchange. In 1983 it started a stock market index, called the EOE index, consisting of the 25 largest companies that trade on the stock exchange. Forward contracts, options, and other sophisticated instruments were traded on the Amsterdam Stock Exchange well before this.

In 1997 the Amsterdam Stock Exchange and the EOE merged, and its blue chip index was renamed AEX, for “Amsterdam EXchange”. It is now managed by Euronext Amsterdam. On 3 October 2011, Princess Máxima opened the new trading floor of the Amsterdam Stock Exchange.

The former Stock Exchange building was the Beurs van Berlage.

Although it is usually considered to be the first stock market, Fernand Braudel argues that this is not precisely true:

“It is not quite accurate to call [Amsterdam] the first stock market, as people often do. State loan stocks had been negotiable at a very early date in Venice, in Florence before 1328, and in Genoa, where there was an active market in the luoghi and paghe of Casa di San Giorgio, not to mention the Kuxen shares in the German mines which were quoted as early as the fifteenth century at the Leipzig fairs, the Spanish juros, the French rentes sur l’Hotel de Ville (municipal stocks) (1522) or the stock market in the Hanseatic towns from the fifteenth century. The statutes of Verona in 1318 confirm the existence of the settlement or forward market … In 1428, the jurist Bartolomeo de Bosco protested against the sale of forward loca in Genoa. All evidence points to the Mediterranean as the cradle of the stock market. But what was new in Amsterdam was the volume, the fluidity of the market and publicity it received, and the speculative freedom of transactions.”

— Fernand Braudel (1983) __

However, it is the first incarnation of what we could today recognize as a stock market.

The Amsterdam Bourse, an open-air venue, was created as a commodity exchange in 1530 and rebuilt in 1608. Rather than being a bazaar where goods were traded intermittently, exchanges had the advantage of being a regularly meeting market, which enabled traders to become more specialized and engage in more complicated transactions. As early as the middle of the sixteenth century, people in Amsterdam speculated in grain and, somewhat later, in herring, spices, whale-oil, and even tulips. The Amsterdam Bourse in particular was the place where this kind of business was carried on. This institution as an open-air market in Warmoestreet, later moved for a while to the ‘New Bridge,’ which crosses the Damrak, then flourished in the ‘church square’ near the Oude Kerk until the Amsterdam merchants built their own exchange building in 1611. Transactions had to be logged into the official accounts book in the East India house, indeed trading was highly sophisticated. Early trading in Amsterdam in the early 16th century (1560s–1611) largely occurred by the Nieuwe Brug bridge, near Amsterdam Harbor. Its proximity to the harbor and incoming mail made it a sensible location for traders to be the first to get the latest commercial news.

Shortly thereafter, the city of Amsterdam ordered the construction of an exchange in Dam Square. It opened in 1611 for business, and various sections of the building were marked for commodity trading and VOC securities. A bye-law on trade in the city dictated that trade could only take place in the exchange on weekdays from 11 a.m. to noon. While only a short amount of time for trading inside the building, the window created a flurry of investors that in turn made it easier for buyers to find sellers and vice versa. Thus, the building of the stock exchange led to a vast expansion of liquidity in the marketplace. In addition, trading was continued in other buildings, outside of the trading hours of the exchange, such as the trading clubs, and was not prohibited in hours outside of those outlined in the bye-law.

The location of exchange relative to the East India house was also strategic. Its proximity gave investors the luxury of walking a short distance to both register the transaction in the official books of the VOC, and complete the money transfer in the nearby Exchange Bank, also in Dam square.

Brussels (1801–2000)

The Brussels Stock Exchange (French: Bourse de Bruxelles, Dutch: Beurs van Brussel) was founded in 1801 by decree of Napoleon. As part of the covering of the river Senne for health and aesthetic reasons in the 1860s and 1870s, a massive programme of beautification of the city centre was undertaken. Architect Léon-Pierre Suys, as part of his proposal for covering of the Senne, designed a building to become the centre of the rapidly expanding business sector. It was to be located on the former butter market, (itself situated on the ruins of the former Recollets Franciscan convent) on the newly created Anspach Boulevard (then called ‘Central Boulevard’). The building was erected from 1868 to 1873, and housed the Brussels Stock Exchange until 1996. The Bourse is due to become a beer museum and will open to the public in 2018.[36] The building does not have a distinct name, though it is usually called simply the Bourse/Beurs. It is located on Boulevard Anspach, and is the namesake of the Place de la Bourse/Beursplein, which is, after the Grand Place, the second most important square in Brussels. The building combines elements of the Neo-Renaissance and Second Empire architectural styles. It has an abundance of ornaments and sculptures, created by famous artists, including the brothers Jacques and Joseph Jacquet, Guillaume de Groot, French sculptor Albert-Ernest Carrier-Belleuse and his then-assistant Auguste Rodin.

Paris (1724–2000)

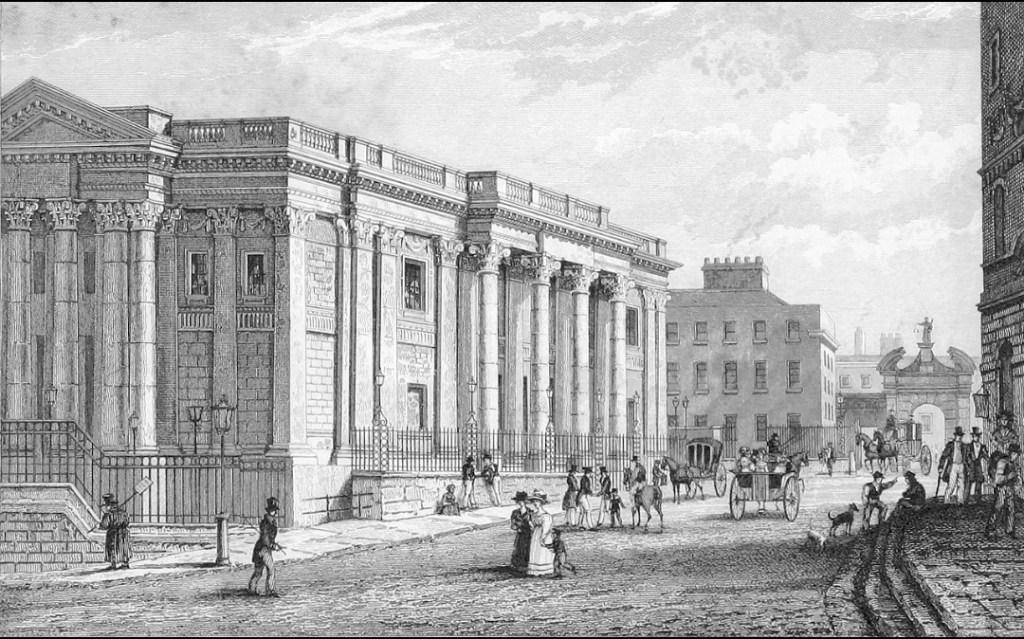

The Paris Stock Exchange (French: Bourse de Paris) was located in Palais Brongniart in the Place de la Bourse, in the II arrondissement, Paris. Historically, stock trading took place at several spots in Paris, including rue Quincampoix, rue Vivienne (near the Palais Royal), and the back of the Opéra Garnier (the Paris opera house).

In the early 19th century, the Paris Bourse’s activities found a stable location at the Palais Brongniart, or Palais de la Bourse, built to the designs of architect Alexandre-Théodore Brongniart from 1808 to 1813 and completed by Éloi Labarre from 1813 to 1826

Brongniart had spontaneously submitted his project, which was a rectangular neoclassical Roman temple with a giant Corinthian colonnade enclosing a vaulted and arcaded central chamber. His designs were greatly admired by Napoleon and won Brongniart a major public commission at the end of his career. Initially praised, the building was later attacked for academic dullness. The authorities had required Brongniart to modify his designs, and after Brongniart’s death in 1813, Labarre altered them even further, greatly weakening Brongniart’s original intentions. From 1901 to 1905 Jean-Baptiste-Frederic Cavel designed the addition of two lateral wings, resulting in a cruciform plan with innumerable columns. According to the architectural historian Andrew Ayers, these alterations “did nothing to improve the reputation of this uninspiring monument.”

From the second half of the 19th century, official stock markets in Paris were operated by the Compagnie des agents de change, directed by the elected members of a stockbrokers’ syndical council. The number of dealers in each of the different trading areas of the Bourse was limited. There were around 60 agents de change (the official stockbrokers). An agent de change had to be a French citizen, be nominated by a former agent or his estate, and be approved by the Minister of Finance, and he was appointed by decree of the President of the Republic. Officially, the agents de change could not trade for their own account nor even be a counterpart to someone who wanted to buy or sell securities with their aid; they were strictly brokers, that is, intermediaries. In the financial literature, the Paris Bourse is hence referred to as order-driven market, as opposed to quote-driven markets or dealer markets, where price-setting is handled by a dealer or market-maker. In Paris, only agents de change could receive a commission, at a rate fixed by law, for acting as an intermediary. However, parallel arrangements were usual in order to favor some clients’ quote[clarification needed]. The Commodities Exchange was housed in the same building until 1889, when it moved to the present Bourse de commerce. Moreover, until about the middle of the 20th century, a parallel market known as “La Coulisse” was in operation.

Until the late 1980s, the market operated as an open outcry exchange, with the agents de change meeting on the exchange floor of the Palais Brongniart. In 1986, the Paris Bourse started to implement an electronic trading system. This was known generically as CATS (Computer Assisted Trading System), but the Paris version was called CAC (Cotation Assistée en Continu). By 1989, quotations were fully automated. The Palais Brongniart hosted the French financial derivatives exchanges MATIF and MONEP, until they were fully automated in 1998.

Lisbon (1769–2002)

The predecessor of the Lisbon Stock Exchange (Portuguese: Bolsa de Valores de Lisboa) was created in 1769 as the Assembleia dos Homens de Negócio (Assembly of Businessmen) in the Commerce Square, in downtown Lisbon. In 1891, the Bolsa de Valores do Porto (Oporto Stock Exchange) in Oporto was founded.

After the military coup on April 25, 1974, both the Lisbon and Porto stock exchanges were closed by the revolutionary National Salvation Junta (they would be reopened a couple of years later).

At the end of 2001, 65 companies were listed on BVLP-regulated markets, representing a market capitalization of Euro 96.1 billion. From January to December 2001, a total of 4.7 million futures and options contracts were traded on the BVLP market.

The Euronext Lisbon was formed in 2002 when the shares of Bolsa de Valores de Lisboa e Porto (BVLP) were acquired by Euronext and the exchange was merged into the pan-European exchange. BVLP, the Portuguese exchange, was formed in the 1990s restructuring of the Lisbon Stock Exchange association and the Porto Derivatives Exchange Association.

Dublin (1799–2018)

The Irish Stock Exchange (ISE; Irish: Stocmhalartán na hÉireann) was first recognised by legislation in 1799 when the Irish Parliament passed the Stock Exchange (Dublin) Act. In different periods in its history, the ISE included a number of regional exchanges, including the Cork and Dublin exchanges. The first woman to be admitted to a stock exchange was, Oonah Keogh to the Dublin Stock Exchange in 1925. In 1973, the Irish exchange merged with British and other Irish stock exchanges becoming part of the International Stock Exchange of Great Britain and Ireland (now called the London Stock Exchange).

In 1995, it became independent again and in April 2014 it demutualised changing its corporate structure and becoming a plc which is owned by a number of stockbroking firms.

At the time of its demutualisation the country’s main stockbrokers received shares in the €56m-valued exchange and dividing up €26m in excess cash. Davy Stockbrokers took the largest stake, at 37.5 per cent, followed by Goodbody Stockbrokers with 26.2 per cent; Investec with 18 per cent; the then Royal Bank of Scotland Group 6.3 per cent; Cantor Fizgerald 6 per cent; and Campbell O’Connor with 6 per cent.

In March 2018, Euronext completed the purchase of the ISE, and renamed the ISE as Euronext Dublin.

Oslo (1818–2019)

Oslo Børs was established by a law of September 18, 1818. Trading on Oslo Børs commenced on April 15, 1819. In 1881 Oslo Børs became a stock exchange, which means securities were listed. The first listing of securities contained 16 bond series and 23 stocks, including the Norwegian central bank (Norges Bank). Oslo Børs cooperates with London Stock Exchange on trading systems. The exchange has also a partnership with the stock exchanges in Singapore and Toronto (Canada) for a secondary listing of companies. The stock exchange was privatized in 2001, and is, after the merger in 2007, 100% owned by Oslo Børs VPS Holding ASA.

The over 180-year-old stock exchange building has been the subject of many long debates about how the building should be managed and designed over the years. Several of Christiania’s (the name of Oslo between 1624 and 1925) best known business men fought for years to get approved and funded the construction of a stock exchange in Christiania, the capital of Norway from 1814.

In 1823 a building committee was appointed to consider the various suggested drawings at the time. The committee chose the architect Christian H. Grosch’s proposal. On July 14, 1826 the Ministry approved the final plans of drawings and budgets. In 1828 it was called Norway’s first monumental building, completed on the site called Grønningen, the first public park in Christiania.

Oslo Børs Holding ASA was the holding company that owned Oslo Stock Exchange of Norway from 2001 to 2008.

The company was created in 2001 when the Oslo Stock Exchange was converted from a self-owning institution to a public limited company. The ownership of Oslo Børs Holding was spread out between a large number of owners, the largest being DnB NOR (18%). The Nordic stock exchange group OMX held a 10% stake as well. The company was not publicly listed. In 2008 it merged with Verdipapirsentralen ASA (VPS) to create the new holding company Oslo Børs VPS Holding ASA.

Oslo Børs Holding had two subsidiaries, Oslo Børs ASA that operates the stock exchange and Oslo Børs Informasjon AS that manages the information systems of the exchange.

2000–2001: Founding

Euronext was formed on 22 September 2000 following a merger of the Amsterdam Stock Exchange, Brussels Stock Exchange, and Paris Bourse, in order to take advantage of the European Union’s (EU) single currency and harmonisation of financial markets.

2001–2007: First round of European acquisitions

In December 2001, Euronext acquired the shares of the London International Financial Futures and Options Exchange (LIFFE), forming Euronext.LIFFE. In 2002 the group merged with the Portuguese stock exchange Bolsa de Valores de Lisboa e Porto (BVLP), renamed Euronext Lisbon. In 2001, Euronext became a listed company itself after completing its initial public offering.

In 2003, Euronext cash products were integrated onto a single platform (NSC).

In 2004, Euronext derivatives products were integrated onto LIFFE CONNECT.

In 2005, Euronext introduced Alternext as a market segment to help finance small and mid-class companies in the Eurozone.

2007–2012: Merger with the New York Stock Exchange

Due to apparent moves by NASDAQ to acquire the London Stock Exchange or Euronext itself, NYSE Group, owner of the New York Stock Exchange (NYSE), offered €8 billion (US$10.2b) in cash and shares for Euronext on 22 May 2006, outbidding a rival offer for the European Stock exchange operator from Deutsche Börse, the German stock market. Contrary to statements that it would not raise its bid, on 23 May 2006, Deutsche Börse unveiled a merger bid for Euronext, valuing the pan-European exchange at €8.6 billion (US$11b), €600 million over NYSE Group’s initial bid.[50] Despite this, NYSE Group and Euronext penned a merger agreement, subject to shareholder vote and regulatory approval. The initial regulatory response by SEC chief Christopher Cox (who was coordinating heavily with European counterparts) was positive, with an expected approval by the end of 2007.

Deutsche Börse dropped out of the bidding for Euronext on 15 November 2006, removing the last major hurdle for the NYSE Euronext transaction. A run-up of NYSE Group’s stock price in late 2006 made the offering far more attractive to Euronext’s shareholders. On 19 December 2006, Euronext shareholders approved the transaction with 98.2% of the vote. Only 1.8% voted in favour of the Deutsche Börse offer. Jean-François Théodore, the chief executive officer of Euronext, stated that they expected the transaction to close within three or four months. Some of the regulatory agencies with jurisdiction over the merger had already given approval. NYSE Group shareholders gave their approval on 20 December 2006. The merger was completed on 4 April 2007, forming NYSE Euronext.

The new firm, NYSE Euronext, was headquartered in New York City, with European operations and its trading platform run out of Paris. Then-NYSE CEO John Thain, who was to head NYSE Euronext, intended to use the combination to form the world’s first global stock market, with continuous trading of stocks and derivatives over a 21-hour time span. In addition, the two exchanges hoped to add Borsa Italiana (the Milan stock exchange) into the grouping.

In 2008 and 2009 Deutsche Börse made two unsuccessful attempts to merge with NYSE Euronext. Both attempts did not enter into advanced steps of merger. In 2011, Deutsche Börse and NYSE Euronext confirmed that they were in advanced merger talks. Such a merger would create the largest exchange in history. The deal was approved by shareholders of NYSE Euronext on July 7, 2011, and Deutsche Börse on July 15, 2011 and won the antitrust approved by the US regulators on December 22, 2011. On February 1, 2012, the deal was blocked by European Commission on the grounds that the new company would have resulted in a quasi-monopoly in the area of European financial derivatives traded globally on exchanges. Deutsche Börse unsuccessfully appealed this decision.

In 2012, Euronext announced the creation of Euronext London to offer listing facilities in the UK. As such, Euronext received in June, 2014 Recognized Investment Exchange (RIE) status from Britain’s Financial Conduct Authority.

2012–2014: Acquisition by Intercontinental Exchange

On 20 December 2012, the boards of directors of both Intercontinental Exchange (ICE) and the NYSE Euronext approved an $8 billion acquisition of NYSE Euronext. Under the terms shareholders of NYSE would receive either $33.12 in cash for each share or .2581 IntercontinentalExchange Inc. shares, or a combination of $11.27 in cash per share plus .1703 shares of stock. The acquisition is subject to regulator approval, though since the operations of ICE and NYSE have little in common—ICE is largely devoted to trading commodities as opposed to NYSE’s business of trading stocks and securities—the deal is not expected to be blocked. ICE said that after the deal closed it would sell the Euronext portion of the company, including stock exchanges in Amsterdam, Brussels, Lisbon and Paris. The deal went through and Euronext is a sister division to NYSE and part of ICE. ICE CEO Jeffrey C. Sprecher would continue in that position at the combined company, while NYSE CEO Duncan Niederauer would serve as president.[66] The future of the New York Stock Exchange’s historic trading floor under ICE has not been announced. ICE closed the high profile and historic trading floors of its other earlier acquisitions, the International Petroleum Exchange and the New York Board of Trade in New York.

In December 2012 Intercontinental Exchange (ICE) announced plans to acquire NYSE Euronext, owner of Euronext, in an $8.2 billion takeover.

In May 2013, Euronext established Enternext as a subsidiary to help small and medium-size enterprises (SMEs) listed on Euronext outline and apply a strategy most suited to support their growth.

The ICE’s deal was approved by the shareholders of NYSE Euronext and Intercontinental Exchange on June 3, 2013. The European Commission approved the acquisition on 24 June 2013 and on Aug. 15, 2013 the US regulator, SEC, granted approval of the acquisition. European regulators and ministries of Finance of the participating countries approved the deal and on November 13, 2013 the acquisition was completed.

2014–2017: Re-emergence

Part of ICE’s deal to acquire NYSE Euronext was a spin-off for Euronext, which was considered a positive element for European stakeholders. After a complex series of operations, this occurred on 20 June 2014, through an initial public offering (IPO). The former Euronext.LIFFE was retained by ICE and renamed ICE Futures Europe. In order to stabilise Euronext, a consortium of eleven investors decided to invest in the company as “reference shareholders”. These investors owned 33.36% of Euronext’s capital and have a 3 years lockup period: Euroclear, BNP Paribas, BNP Paribas Fortis, Société Générale, Caisse des Dépôts, BPI France, ABN Amro, ASR, Banco Espirito Santo, Banco BPI and Belgian holding public company Belgian Federal Holding and Investment Company [fr] (SFPI/FPIM). They have 3 board seats.

In June 2014, EnterNext launched two initiatives to boost SME equity research and support the technology sector. EnterNext partnered with Morningstar to increase equity research focusing on mid-size companies, especially in the telecommunications, media and technology (TMT) sector.

On 22 September 2014, Euronext announced a partnership with DEGIRO regarding the distribution of retail services of Euronext. Upon publishing the third quarter results for 2014, the partnership was seen as a plan for Euronext to compete more effectively on the Dutch retail segment.

In May 2017, Alternext was renamed to Euronext Growth.

2017–present: Second round of European acquisitions Edit

On 14 August 2017, Euronext announced the completion of its acquisition of FastMatch, a currency trading platform.

On 27 March 2018, Euronext announced the completion of its acquisition of the Irish Stock Exchange.

On 18 June 2019, Euronext announced the completion of its acquisition of the Oslo Stock Exchange.

On 5 December 2019, Euronext announced that it would acquire 66% of the European power exchange Nord Pool. The acquisition was completed on 15 January 2020.

On 23 April 2020, Euronext announced that it would acquire ca. 70% of the Danish Central Securities Depository, VP Securities. The acquisition was completed on 4 August 2020.

On 18 September 2020, the London Stock Exchange Group (LSEG) entered into exclusive talks to sell the Italian Bourse (formally 100% of London Stock Exchange Group Holdings Italia S.p.A.), situated in Milan, to Euronext. As part of the deal, CDP Equity, 100% owned by Cassa Depositi e Prestiti, and Intesa Sanpaolo would become Euronext shareholders. LSEG is selling Italian Bourse as part of regulatory remedies to see through its $27 billion purchase of data provider Refinitiv. A €4.3 bn deal was announced on 9 October, albeit contingent on the European Commission formally stating in mid-December that it will only permit LSEG’s acquisition of Refinitiv if the Italian Bourse is sold. Euronext’s acquisition is expected to be completed in the first half of 2021